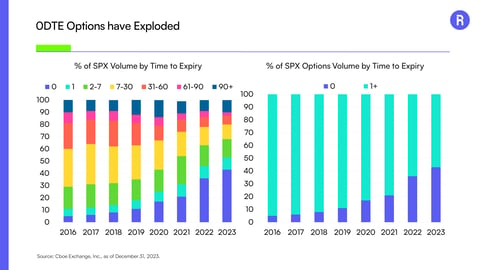

Roundhill Roundup: The Degen Economy 0DTE Options. Meme Coins. Parlay Bets. What do these three have in common? The growth of 0DTE (zero... Read More →

There’s More to Generative AI than Nvidia, Why Active for AI Exposure Generative AI has the potential to be as transformative as the introduction of the internet was in... Read More →

How to Invest in Luxury Stocks: The Complete Beginners Guide Luxury goods is one sector that has performed consistently well over recent decades, despite the... Read More →

How to Invest in Cannabis: The Complete Beginners Guide The legalization of cannabis for both medicinal and recreational purposes in various jurisdictions,... Read More →

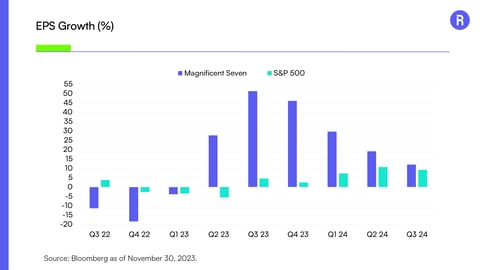

Roundhill Roundup: When Seven Means Hundreds Through the first two months of the year, the Magnificent Seven Stocks have returned 14%, while... Read More →

How to Invest in AI: The Complete Beginners Guide Artificial Intelligence, commonly known as AI, is all set to transform our daily lives. As with... Read More →

Roundhill Roundup: Sell the News = Range Bound Crypto The widespread anticipation for the approval of spot bitcoin ETFs concluded with a paradoxical... Read More →

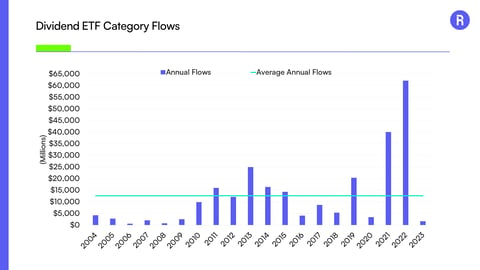

Dividends in the Doghouse A recent Bloomberg News article highlighted how flows into U.S.-listed dividend exchange-traded... Read More →

Identifying the Key Themes of 2024 Thematic investing is about identifying trends and being willing to try to see into the future.... Read More →

The RIC Advantage: Exploring Tax Benefits in ETF Structuring What is a RIC? Nearly all exchange-traded funds (ETFs) elect to be treated as RICs, or Regulated... Read More →

The BIG Picture - Why the Magnificent Seven are Magnificent At this point, everyone knows that seven stocks have contributed nearly all (73% to be exact) of... Read More →

How to (and How Not to) Gain Exposure to the Magnificent Seven Why Precision Matters Investing with precision is critical. When it comes to exchange-traded funds,... Read More →

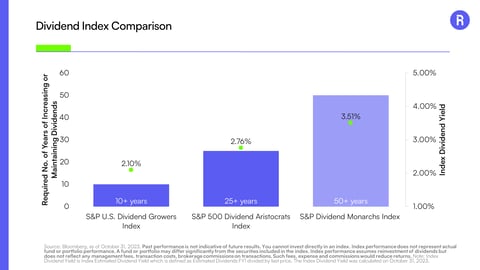

Introducing KNGS: Crowning a New King With the launch of the S&P Dividend Monarchs Index, there may be a new king in town when it comes... Read More →

Dividend Monarchs – 50+ Years of Consecutive Dividend Increases Dividend Monarchs, sometimes referred to as Dividend Kings, refers to the small group of stocks... Read More →

The BIG Picture - More of the Same Means More Magnificence… For Now Investors came into October hoping that the start of the fourth quarter would bring them some... Read More →