At the end of 2023, market prognosticators forecasted that 2024 would be a year of broadening, a prediction that smaller capitalization stocks would outperform mega-caps stocks such as the Magnificent Seven. Instead, 2024 bucked the trend with the Magnificent Seven posting a 73% total return through December 12. Equity markets reflected a definitive “winner takes all” environment with equity leadership catalyzed by companies exhibiting positive operating leverage.

With 2025 fast approaching, a new year will bring about a new U.S. presidential administration and a constantly evolving macroeconomic environment. In our view, a fair number of 2024’s dominant market themes have the durability to influence 2025’s market behavior. To illustrate these enduring themes and their potential implications for the coming year, we have curated a selection of essential charts derived from Roundhill’s actionable thematic ETF suite.

Magnificent Seven

The Magnificent Seven have demonstrated noteworthy dominance and leadership in 2024. Despite a correction from record levels in July, the group has shown remarkable resilience and appears poised to end the year on a strong note. A closer look at the impressive year-to-date total returns reveals that each member contributed to the group’s surge. NVDA has been the standout, adding over $2 trillion in market cap, while TSLA has “only” contributed a little over $500 billion, the smallest of the group. We believe their leadership in the equity market is sustainable, driven by their economies of scale, exposure to generative artificial intelligence, and ability to capitalize on positive operating leverage.

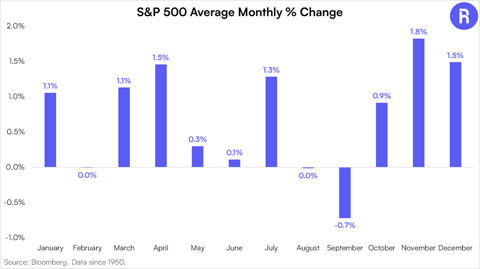

Market Volatility

2022’s bear market led to a historically elevated share of trading days with a greater than 1% intraday trading range in a calendar year. As equity markets rallied off of October 2022’s low, intraday volatility fell. To-date, roughly 30% of 2024’s trading days have registered a 1%+ trading range, comparable to 2019’s tally, but not the extremes of 2017.

Generative Artificial Intelligence

In our view, the durable impacts of generative artificial intelligence (AI) have not yet reached the market. On balance, a majority of the industry, including the Magnificent Seven, remains in spend mode, investing in research and development (R&D) efforts dedicated to various AI initiatives. As the aggregate sum of invested cash in AI climbs, so has the mentions of “AI” in S&P 500 company transcripts. Investor enthusiasm is clear, and it is apparent that corporations are putting their money where their mouth is.

China

Earlier this year, the People’s Bank of China (PBOC) announced various monetary stimulus measures to fuel the economy and improve consumer confidence while in pursuit of its 5% growth target. More recently, China's Politburo, or the Political Bureau of the Communist Party of China (CPC), pledged that more easing was on the way. If this time is indeed different, a targeted way to play China’s imminent stimulus could be a group of Chinese innovators that we have dubbed the “China Dragons.” Tencent, Pinduoduo, Alibaba, Meituan, BYD, Xiaomi, JD.com, Baidu, and NetEase have collectively exhibited noteworthy net income growth, vastly outpacing Chinese large-cap peers.

GLP-1 & Weight Loss Drugs

The weight loss and GLP-1 drug landscape is rapidly evolving. Novo Nordisk (NVO), with Ozempic and Wegovy, and Eli Lilly (LLY), with Zepbound and Mounjaro, have established themselves as clear leaders in the weight loss drug market. Can their dominance endure? The pipeline of weight loss and GLP-1 drugs continues to expand, with over 130 drugs currently in clinical studies at various stages of development. Of these, 11.5% are in Phase III, 44.6% in Phase II, and 43.9% in Phase I. In our view, navigating this dynamic environment will continue to require an active investment approach.

Sports Betting & iGaming

The legalization of sports betting has continued to gain momentum in the United States. In 2024, Vermont and North Carolina both commenced online sports betting operations. Meanwhile, Missouri narrowly passed a ballot measure to legalize sports betting in recent voting. 38 states, as well as Washington D.C., now permit sports betting. Since June 2018, the legal sports betting industry has generated roughly $36 billion in aggregate cumulative revenue.

Video Games

Grand Theft Auto V, published by Rockstar Games under Take-Two Interactive (TTWO), is one of the best selling games of all-time. GTA V has sold 205 million copies since its release in September 2013. The next installment of the series, Grand Theft Auto VI, is expected to be released in the second half of 2025. Wall Street analyst ratings reflect anticipation and excitement for the game’s reception. TTWO currently has 27 buy ratings of 31 total ratings, 87.1% of total coverage. 2025 is gearing up to be a major year for the videogame industry.

Cannabis

The perception of cannabis and public opinion on its legality has changed drastically over the decades. In a recent Gallup poll, 68% of respondents said that they believed the use of marijuana should be legal. The current administration has worked towards rescheduling marijuana from schedule I to schedule III, but the process is ongoing. That said, revenue for the industry continues to show growth. According to the BDSA, 2023 U.S. cannabis sales totaled $29.5 billion, with $32.4 billion expected for 2024. Looking ahead, the U.S. could achieve $46 billion in cannabis sales by 2028, commanding a majority of the $58 billion in estimated global legal sales.

Crypto

Bitcoin and ether have seen a rapidly improving regulatory backdrop develop in the U.S. In January 2024, the first U.S. listed spot bitcoin exchange traded funds (ETFs) began trading, followed by spot ether ETFs in July. The listing and trading of options on select spot bitcoin ETFs began in November. Meanwhile, the incoming U.S. administration has signaled their support for crypto and its mainstream adoption. Taken together, these signs have catalyzed a surge of inflows into spot bitcoin ETFs with $8.6 billion having piled in over the 20 trading days ending December 13th. While this sentiment could provide some short-term mean reversion risk for investors, excitement for crypto’s future is blossoming and appears here to stay.

This information is provided solely as general investment education. None of the information provided should be regarded as a suggestion to engage in or refrain from any investment related course of action. Investing involves risk, loss of principal is possible.

Not an offer: This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact 1-855-561-5728 or consult with the professional advisor of their choosing.

Forward-looking statements: Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Use of Third-party Information: Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Roundhill Financial Inc. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Roundhill Financial Inc. or any other person. While such sources are believed to be reliable, Roundhill Financial Inc. does not assume any responsibility for the accuracy or completeness of such information. Roundhill Financial Inc. does not undertake any obligation to update the information contained herein as of any future date.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index.

Except where otherwise indicated, the information contained in this presentation is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision. The performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted.