Taylor Swift’s anthem “Shake It Off” captured the mood this quarter as stocks shrugged off one scary headline after another and kept marching higher.

Stocks Shaking It Off

If you spent Q2 doom‑scrolling tariff posts and fretting over macro “what‑ifs,” the market had a simple response: watch me shake it off. From the tariff scare in early April to “Big, Beautiful Bill” budget brinkmanship in June, headline risk felt relentless, yet buyers were even more persistent. Over just 89 volatile days, stocks logged a v-shaped recovery, transitioning from a bear market into fresh all‑time highs.

Why the resilience? Cash‑flush megacaps kept churning out record earnings, AI demand showed no sign of cooling, and every incremental hint of trade détente added fuel to risk appetite. History also reminds us that the largest daily gains tend to cluster around the worst‑looking news flow with April 9’s 9.5% surge (third‑largest since 1950) was the latest reminder.

The bottom line? Time in the market beats timing the market.

Macro Snapshot - What Happened & What’s Ahead

-

S&P 500 +10.6% in 2Q 2025 → 35ᵗʰ strongest quarter since 1950.

-

Stocks rallied nearly 30% off the April 7 low as trade rhetoric softened and growth hung in.

-

89-day round-trip for the S&P 500: 33 days down (Feb 19 → Apr 7) and 56 days back to new highs (Jun 27).

-

April 9 spike was the 3ʳᵈ largest daily gain since 1950.

-

Fed policy watch: Futures are pricing a small but improving chance of a Fed cut at the July 30 meeting as core inflation drifts closer to 2%.

A full calendar of economic shocks in the first six months of the year have not deterred the financial markets. On a price return basis, the S&P 500 is up nearly 6% year-to-date and up 9% between the calendar of Trade & Policy Updates below (May 8th-July 1st).

Uncertainty Breeds Opportunity

If 2Q’25 has reminded investors of one market maxim, it is that uncertainty breeds opportunity. Amid a historic rally off the April 7 market low, the U.S. Categorical Economic Policy Uncertainty Index for National Security surged to a new record for the month of April. With the world possibly entering an era of deglobalization and Israel-Iran war risking global spillover, how could the global equity markets be trading to record highs?

Historically, prior surges in the National Security Policy Uncertainty Index exceeding the 95th percentile of all readings since 1985 have tended to bullish for the S&P 500. Following such observations, the S&P 500 has averaged 1.9%, 4.7%, 8.3% and 15.3% over the next one, three, six, and twelve months respectively, outpacing historical average rates of return.

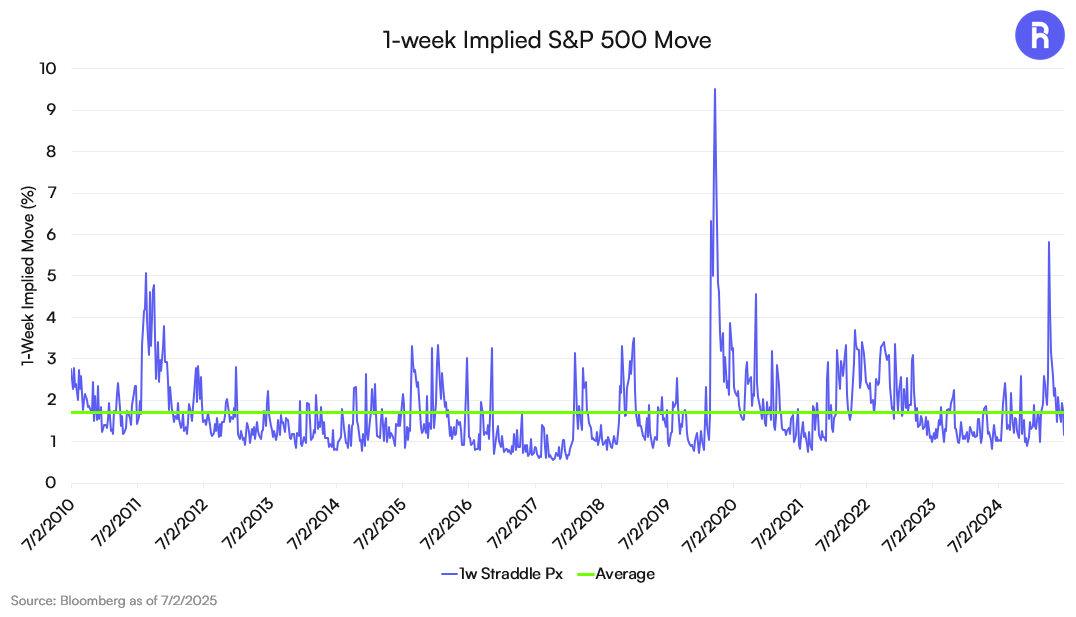

Comparing the historical chart of Economic Policy Uncertainty to implied S&P 500 weekly moves, which have been derived from option markets, equity markets are indeed “shaking it off”. Despite policy uncertainty still trading near the 95th percentile, the implied 1-week move in the S&P 500 is only trading in the 28th percentile. Not only are markets not reactive to policy uncertainty, they are also not proactively pricing in any response.

Conclusion — “Players Gonna Play”

As Taylor Swift reminds us, “while you’ve been getting down and out about the liars and the dirty, dirty cheats of the world,” the market kept cruising. Swifties know the strategy: shake it off and stay in the game because missing the concert’s hottest track (think April 9) hurts more than enduring a few off-key notes along the way.

Yet even after this blockbuster first half, our May 2025 Roundhill Roundup called for a fat and flat year: modest index‑level progress book‑ended by sharp, episodic swings as policy, earnings, and geopolitics trade the spotlight. We still see that script playing out, so be ready to shake it off whenever volatility drops a surprise beat.

Investor Takeaways

-

Stay invested. Missing “monster” up days can erase months of outperforming tweaks.

-

Lean into secular growth. AI, cloud, and robotics remain multi-year demand stories.

-

Hold dry powder. Volatility spikes around policy deadlines (July 9 tariffs, July 30 Fed) can create entry points.

This information is provided solely as general investment education. None of the information provided should be regarded as a suggestion to engage in or refrain from any investment related course of action. Investing involves risk, loss of principal is possible.

Not an offer: This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact 1-855-561-5728 or consult with the professional advisor of their choosing.

Forward-looking statements: Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Use of Third-party Information: Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Roundhill Financial Inc. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Roundhill Financial Inc. or any other person. While such sources are believed to be reliable, Roundhill Financial Inc. does not assume any responsibility for the accuracy or completeness of such information. Roundhill Financial Inc. does not undertake any obligation to update the information contained herein as of any future date.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index.

Except where otherwise indicated, the information contained in this presentation is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision. The performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted.