Introduction

For decades, bonds were the cornerstone of multi-asset portfolios. Whether used for income generation, downside mitigation, or diversification, fixed income earned its reputation as the dependable anchor to the greater returns and greater risk that come from stocks.

But something has fundamentally changed.

In 2022, when U.S. equities suffered one of their worst annual drawdowns in recent memory, bonds failed to do their job. The Bloomberg U.S. Aggregate Bond Index declined 13%, marking its worst year in history. Long-duration Treasuries fared even worse falling nearly 30%. For the first time in a generation, both legs of the traditional 60/40 portfolio fell in tandem, leaving investors with nowhere to hide.1

That moment was not an anomaly—it was a turning point.

Today, interest rate volatility, structural inflation risk, a declining US dollar, and fiscal uncertainty have fundamentally altered the behavior of bonds. As a result, one of the most entrenched paradigms in investing, the 60/40 portfolio, is breaking down.

Fixed Income: No Longer Defensive, No Longer Reliable

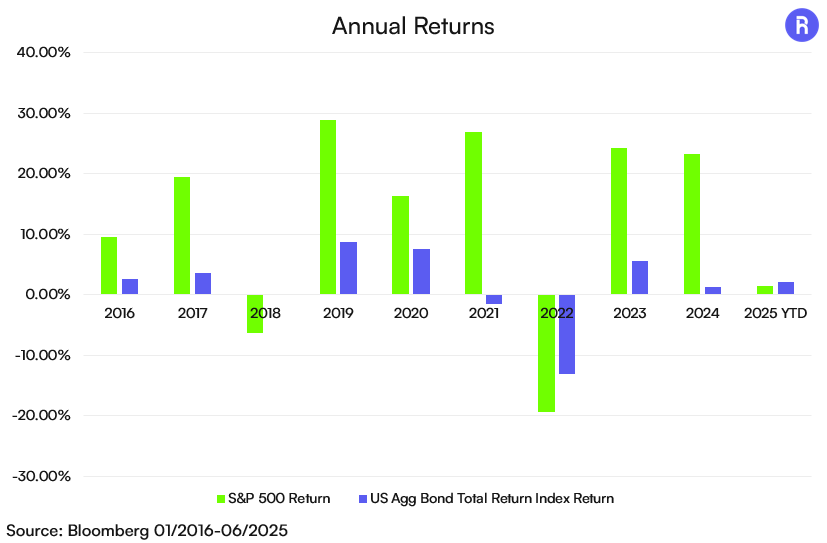

To understand the structural challenges facing bonds, it's useful to look at recent annual returns.

The Bloomberg U.S. Aggregate Bond Index posted back-to-back negative calendar years in 2021 and 2022, in what is supposed to be a defensive asset class. The 13% loss in 2022 marked its worst year on record, and 2023 offered little relief, finishing flat to slightly negative depending on the duration of exposure. These results weren’t just disappointing, they destabilized portfolios built on the assumption that bonds would provide ballast during equity drawdowns.

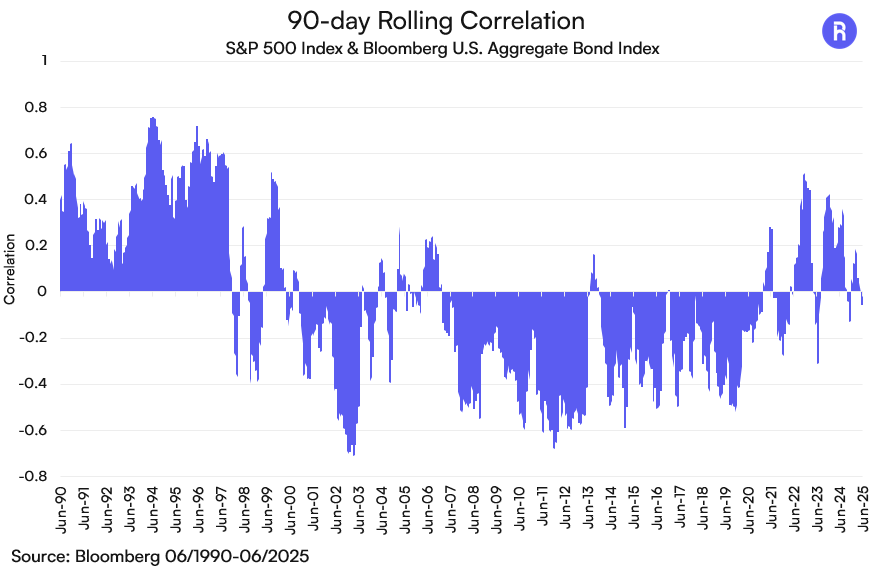

Worse still, bonds have recently failed to hedge portfolios during drawdowns in equities. We tend to think of bonds and equities as having a negative correlation, which yields the diversification benefit that underpins 60/40 construction. This negative correlation was the case for the majority of many years, roughly for the 20 years preceding 2022. In 2022, the stock-bond correlation turned positive and has remained mostly positive since then.

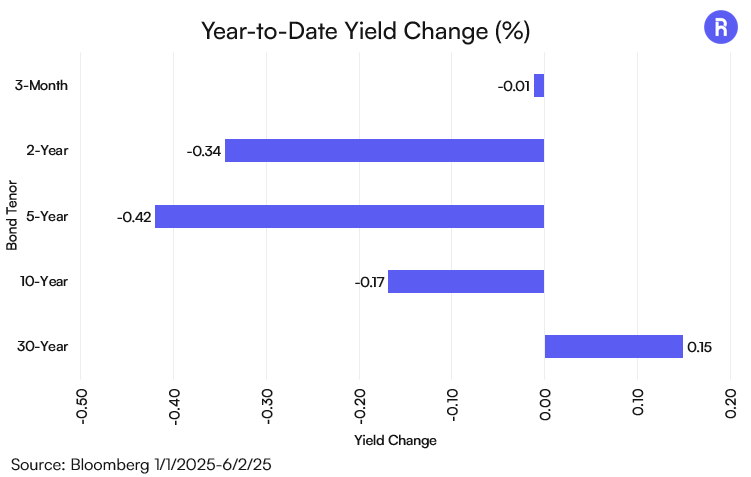

Long Duration Concerns

Despite the recent stabilization in yields, inflation risk remains elevated, particularly as services inflation proves sticky and wage growth continues to outpace productivity. At the same time, term premiums have begun to reprice materially higher, reflecting investor concerns about long-run fiscal sustainability, persistent Treasury issuance, and heightened geopolitical risk premiums. The days of artificially suppressed long-end yields, driven by central bank buying and global disinflation, are behind us. In their place is a more fragile bond market, increasingly vulnerable to both supply-side shocks and deficits that show no sign of narrowing.

Cash as an Alternative

In response, investors have pivoted into ultra-short duration instruments. With Treasury bills and money market funds yielding above 4%, cash allocations have ballooned. As of month-end May 2025, over $6.95 trillion sits in U.S. money market funds, according to ICI.

But this shift presents a new set of challenges:

- Reinvestment risk is elevated if the Fed begins cutting rates in late 2025.

- No capital appreciation potential limits long-term portfolio growth.

- Cash may reduce portfolio volatility, but it comes with the potential erosion of purchasing power over time.

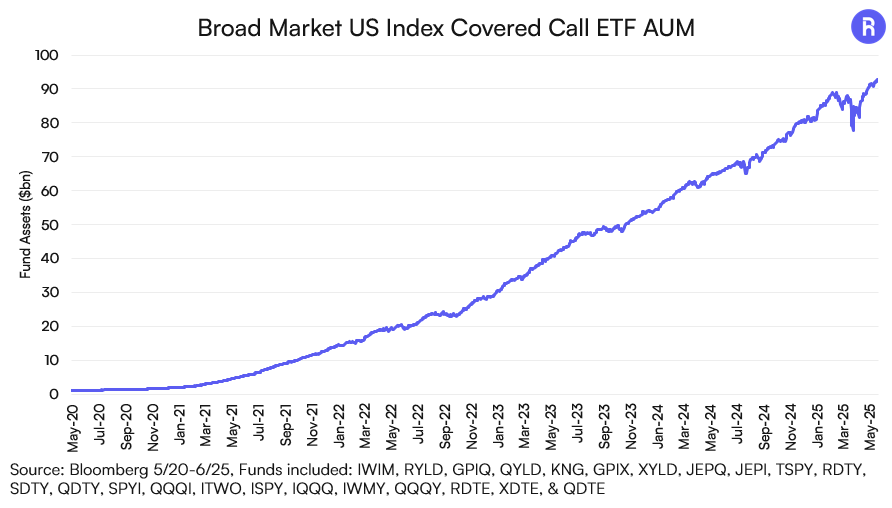

Investors Are Reconstructing the “40” in 60/40

As investors face the reality of diminished bond utility, many are turning to derivatives-based income strategies, particularly covered call ETFs and defined outcome ETFs, as more adaptable tools for portfolio construction.

The Case for Options-Based Income

Covered call strategies allow investors to generate income from equity exposure without relying on bond yields. These strategies benefit from elevated implied volatility, sideways or rangebound equity markets, and increased demand for frequent, consistent income distributions.

Importantly, the structure of many modern income ETFs now offer weekly income distributions, offering greater cash flow regularity, and improved reinvestment flexibility.

While these strategies carry tradeoffs, such as capped upside in strong equity rallies,, their rate-independent income profile makes them attractive in a world where interest rates are no longer a reliable source of return.

Reframing Portfolio Construction: A Modern Income Toolkit

Bonds may not be entirely obsolete, but investors need to reconsider what they expect from them. The defensive, income-generating role that bonds used to fill is increasingly being replaced by:

- Cash for short-term stability

- Covered call strategies for income and equity participation

- Alternatives like gold or crypto designed to operate outside the constraints of US interest rate cycles

Final Thoughts

The question is not whether investors should abandon bonds, it is whether they should rely on them the way they used to.

With real yields compressed, duration risk elevated, and correlations to equities unstable, bonds may have lost their structural advantage in multi-asset portfolios. Investors who continue to depend solely on them for income and diversification are taking risks they may not fully understand.

At Roundhill, we believe in building the modern income toolkit, one that includes option-driven ETFs with frequent distributions, rate-independent return profiles, and adaptability across market regimes. Bonds may have broken down, but your portfolio doesn’t have to.

1 Source: Bloomberg as of 6/6/2025

Disclosures

This information is provided solely as general investment education. None of the information provided should be regarded as a suggestion to engage in or refrain from any investment related course of action. Investing involves risk, loss of principal is possible.

Not an offer: This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact 1-855-561-5728 or consult with the professional advisor of their choosing.

Forward-looking statements: Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Use of Third-party Information: Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Roundhill Financial Inc. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Roundhill Financial Inc. or any other person. While such sources are believed to be reliable, Roundhill Financial Inc. does not assume any responsibility for the accuracy or completeness of such information. Roundhill Financial Inc. does not undertake any obligation to update the information contained herein as of any future date.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index.

Except where otherwise indicated, the information contained in this presentation is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision. The performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance data quoted.